Renting vs. Buying: Why Renting Could Be the Better Option

Does the classic American dream still exist? You know, the one where you must buy a house with a white picket fence to live happily ever after? For years, buying a home was considered the ultimate measure of financial success. You weren’t really “keeping up with the Joneses” or successful in life until you were a homeowner. This logic was turned upside down during the housing bubble of 2008, leading many to rethink the benefits of homeownership.

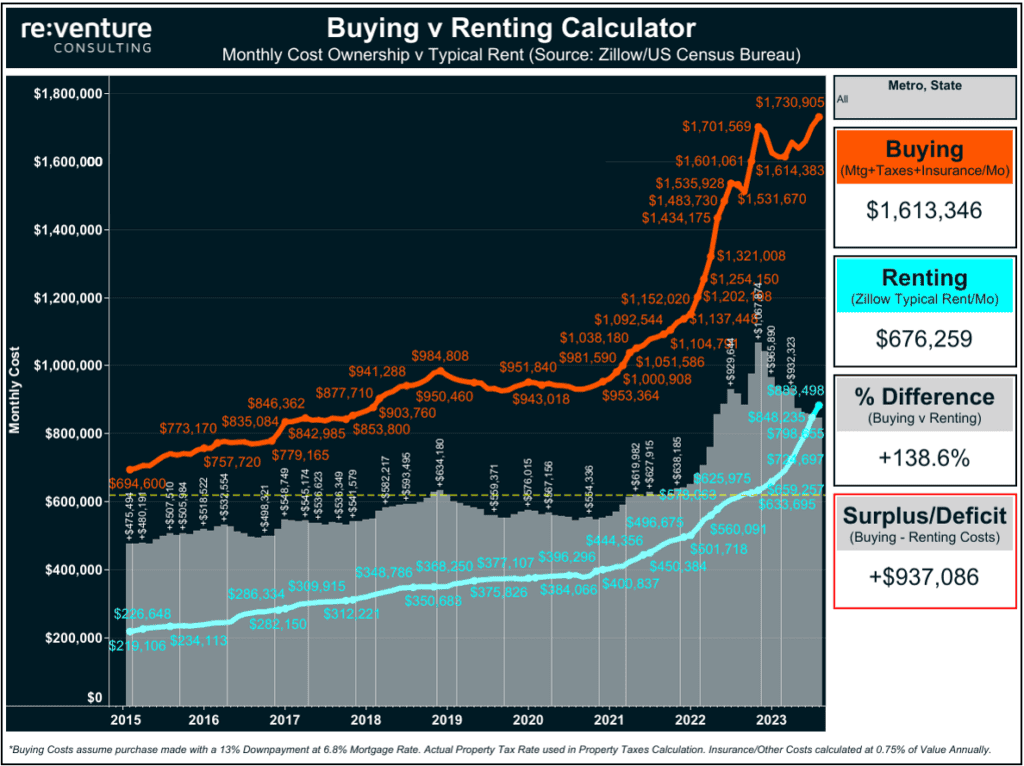

Many people feel pressured into buying a house because they’ve always been told that renting is just throwing money away. “Why pay someone else to live in a house when you could own it yourself?” they say. As financial planners, we often encounter clients who want to purchase a home simply because they feel it’s the right thing to do. But this advice is outdated. Renting offers many benefits that owning a home simply does not. If you’re unsure about buying a home or feel pressured to do so, rest assured that renting can be a great alternative.

Debunking the Homeownership Myth

Buying a Home is an Investment

The loudest argument for buying a home is that it’s an investment. This belief has led people to think that the housing market always goes up in value, allowing them to flip homes and get rich quickly. However, the 2008 financial crisis revealed that these so-called investments can be risky. The housing market crashed, homes were foreclosed on, and many people ended up with nothing. If you had invested that money in the stock market instead, you might have experienced losses, but holding your positions would have eventually led to gains.

Let’s drill down to a single home purchase for personal use. Once you live in a home, it stops being an investment and becomes your primary residence. You bought it because you needed a place to live, and when it no longer serves that purpose, you sell it. There’s a lack of control when it comes to buying and selling your primary residence, so it shouldn’t be thought of as an investment.

Yes, homes typically appreciate to keep up with inflation. You might see higher appreciation in hot real estate markets and flatter appreciation in colder markets. However, any appreciation in your home value often leads to taking out loans or refinancing to tap into that equity. This means the equity is trapped—you can’t really access it without selling your home and rolling it into the next one’s downpayment.

The single biggest reason you can’t think of your home as an investment is due to the negative cash flows it generates. Repair costs, renovation expenses, homeowner association fees, property taxes, private mortgage insurance (PMI), utility fees, and interest all contribute to negative cash flow. When you account for all these costs, you might find that you have a negative return on your home investment. Even if it’s positive, it’s likely less than what the stock market or even inflation could have provided.

The Benefits of Renting

Flexibility

One of the biggest benefits of renting is the flexibility it offers. If you don’t like being tied down in one place or want to keep your options open, renting makes this possible. It can be costly to buy a home only to sell it a few years later, especially if you have to sell it before building up enough equity. Depending on the market, selling a home can take time and might force you to take a loss if you need to move quickly.

Renting also allows you to live in places you might not be able to afford to buy. Real estate can be expensive, especially near downtown areas of major cities. Renting in these locations can make it easier to commute to work and enjoy city life. This can also apply if you’re targeting a specific area for its schools but can’t afford to buy there.

Cost Savings

The costs of buying a home can be daunting. You need money upfront for a down payment and closing costs, which can be a significant hurdle if you’re just starting out. Beyond upfront costs, homes are money pits. Repairs, maintenance, renovations, HOA dues, and property taxes can all add up. As a renter, you’re typically immune from most of these expenses. Yes, you’ll probably have a security deposit upfront, but your ongoing costs are minimal in comparison. Instead of spending that money on a home purchase, you can use that money in other areas of your life, such as maintaining an emergency fund, investing in the stock market, or starting a business.

Not Throwing Money Away

Contrary to what anti-renters say, renting is not throwing money away. You’re paying for a place to live, which is a simple but often overlooked fact. You can also consider the opportunity costs of renting versus buying. Using your money for an emergency fund, starting a business, or investing in the stock market could provide returns equal to or greater than homeownership.

A study by Florida Atlantic University found that “on average, renting and reinvesting wins in terms of wealth creation regardless of property appreciation.” This is because property appreciation is highly correlated with gains in traditional financial assets like stocks and bonds.

Tax Benefits

With changes in tax law, there are now fewer tax benefits to homeownership. The Tax Cuts and Jobs Act raised the standard deduction and put limits on mortgage-related deductions. As a result, many people no longer itemize their tax returns and lose the tax benefits of having a mortgage.

Conclusion

It’s impossible to say definitively that buying is better than renting or vice versa. Both have their merits for different reasons and what works for one person might not work for another. The decision to buy or rent should fit your needs, not because you feel pressured to conform to social norms.

Glossary

Equity: The difference between the market value of your home and the amount you owe on your mortgage.

HOA Dues: Fees paid to a homeowner’s association for the upkeep of common areas and other community services.

Primary Residence: The main home where a person lives.

Refinancing: Replacing an existing mortgage with a new one, typically to get a lower interest rate or access equity.

Stock Market: A marketplace where stocks (shares of ownership in businesses) are bought and sold.

Tax Cuts and Jobs Act (TCJA): A law passed in 2017 that made significant changes to the tax code, including raising the standard deduction and limiting certain deductions.